African Public Debt: A 2025 Retreat Masking Contrasting Realities

| :--- | :--- | |

|---|---|---|

| Botswana | 24.9 | Low |

| Burundi | 13.1 | Moderate |

| Cameroon | 42.7 | Moderate |

| Congo | 19.3 | Low |

| Algeria | 46.2 | Low |

| Benin | 53.4 | Moderate |

| Burkina Faso | 58.6 | High |

| Côte d'Ivoire | 56.8 | Moderate |

| Egypt | 82.9 | High |

| Ghana | 70.5 | Debt Distress |

| Cabo Verde | 109.0 | High |

| Eritrea | 164.0 | Debt Distress |

| Zambia | 78.2 | Debt Distress |

Source: Data compiled from Trading Economics and IMF/World Bank risk classifications, 2024-2025.

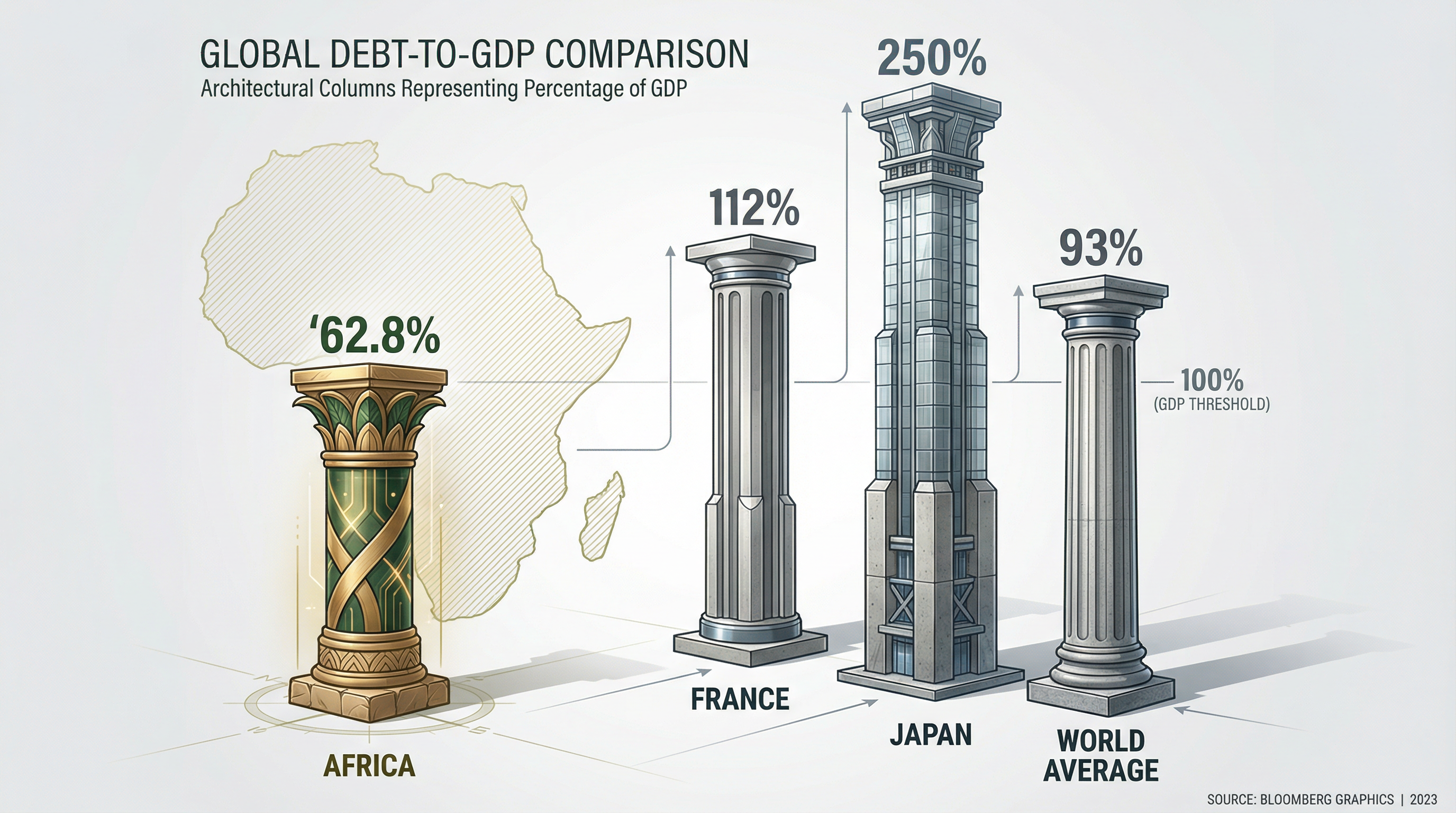

This table highlights several key points. Countries like Botswana and Congo maintain very low debt ratios, reflecting prudent management and sufficient revenues. Conversely, nations such as Eritrea, Cabo Verde, and Ghana significantly exceed, or even explode, the 77% of GDP threshold considered by the IMF as a high-risk indicator for emerging economies. The situation of countries like Ghana and Zambia, officially classified as "in debt distress," has necessitated complex restructuring processes, confirming that the "crisis" is a tangible reality for a minority of countries, but not for the continent as a whole.

From the 1980s SAPs to the 2010s Eurobonds: Three Cycles of Indebtedness

The current situation of African debt is the product of a complex history, marked by several cycles of indebtedness and debt reduction. To understand how we arrived here, a look back is necessary. After independence in the 1960s, many African states resorted to borrowing to finance their development and infrastructure construction. This first wave of borrowing was encouraged by the abundance of liquidity in international financial markets, particularly "petrodollars."

However, the oil shocks of the 1970s, the rise in US interest rates in the early 1980s, and the fall in commodity prices plunged the continent into a severe debt crisis. It was during this period that the International Monetary Fund (IMF) and the World Bank implemented the now-famous Structural Adjustment Programs (SAPs), which conditioned financial aid on drastic economic reforms: privatization, liberalization, and cuts in public spending. These policies, while aiming to restore states' solvency, had very high social costs and left deep scars in collective memory.

A decade later, facing the social failure of SAPs and the unsustainable burden of debt, the international community launched the "Heavily Indebted Poor Countries" (HIPC) initiative in 1996, supplemented by the Multilateral Debt Relief Initiative (MDRI) in 2005. These programs led to the cancellation of a significant portion of the debt of several dozen African countries, bringing the continent's average debt ratio to a historically low level, around 30% of GDP in the early 2010s [5].

This period of calm, however, was short-lived. Taking advantage of very low global interest rates after the 2008 financial crisis and renewed investor appetite for emerging markets, many African countries returned to international financial markets, issuing Eurobonds. The composition of debt then changed radically. While debt was predominantly held by public creditors (states, IMF, World Bank) through the Paris Club, an increasing share is now held by private creditors (banks, investment funds) and new public creditors like China. This diversification of creditors has made debt restructuring coordination much more complex, as demonstrated by the slow negotiations for Zambia or Ghana within the G20's "Common Framework," the successor to the HIPC/MDRI initiatives [6]. The COVID-19 pandemic and the war in Ukraine have only exacerbated vulnerabilities by increasing financing needs and triggering a new rise in global interest rates.

The Debt-to-GDP Ratio Masks the Real Problem: The Cost of Borrowing and Exchange Rate Risk

Focusing solely on the debt-to-GDP ratio, while useful, offers an incomplete and sometimes misleading view of African debt sustainability. The real issue lies less in the overall volume of debt than in its composition and cost, two factors that have changed radically over the past decade and constitute the core of the problem for many countries.

A growing portion of African debt is now denominated in foreign currencies, primarily US dollars. This "dollarization" of debt exposes African economies to significant exchange rate risk. Any depreciation of the local currency against the dollar mechanically increases the burden of debt servicing (interest and principal payments) in local currency, even if the dollar amount remains the same. This phenomenon has been particularly painful for countries like Ghana or Nigeria, whose currencies have fallen sharply in recent years.

Even more problematic is the cost of borrowing. African countries systematically pay higher interest rates than developed countries, even when their economic fundamentals are solid. This "Africa risk premium" is partly fueled by the perceptions and methodologies of international rating agencies (Moody's, S&P, Fitch). Several studies, notably by the United Nations Development Programme (UNDP), have denounced a "perception bias" that costs African countries billions of dollars in excess interest costs. These agencies are criticized for their lack of transparency, their sometimes-delayed responsiveness to economic improvements, and their tendency to apply an almost systematic risk premium to the continent, without sufficiently differentiating national situations. A single downgrade of a country's rating can trigger capital flight and make debt refinancing on the markets nearly impossible or prohibitive.

Finally, debt data does not always capture the full extent of a state's financial commitments. Debts of state-owned enterprises, public-private partnerships (PPPs), or state-guaranteed loans are not always included in public debt statistics, creating hidden fiscal risks. China, which has become a major creditor, also has a practice of often opaque lending, with confidentiality clauses that make it difficult to accurately assess the total indebtedness of certain countries.

Reform of Rating Agencies, IMF SDRs, Fiscal Mobilization: Three Levers Under Discussion

Faced with these challenges, the status quo is no longer tenable. The slight decrease in the debt ratio in 2025 should not mask the urgency of a profound reform of the international financial architecture, a demand increasingly pressed by African leaders. Simple case-by-case restructuring, through mechanisms like the G20 Common Framework, has shown its limits. Slow, complex, and often subject to the geopolitical interests of major creditors, it fails to provide a sustainable and predictable solution for countries in difficulty.

The continent's call focuses on several areas. The first is the reform of rating agencies, to introduce more transparency, competition, and accountability in their assessments, and for their methodologies to more accurately reflect African economic realities. The African Union advocates for the creation of a pan-African rating agency, which could offer an alternative and a counterbalance to the three major agencies that dominate the market today.

The second area is access to fairer and larger-scale financing. This involves increasing the lending capacity of multilateral development banks, such as the African Development Bank (AfDB) and the World Bank. The idea of using IMF Special Drawing Rights (SDRs), international reserve assets, to channel them to developing countries through regional banks is gaining traction. This would provide long-term liquidity at affordable costs to finance investments in infrastructure, energy transition, and human capital.

Finally, a realization is emerging on the continent to strengthen the mobilization of domestic resources. Excessive reliance on external debt is a symptom of an often-too-narrow fiscal base. Improving tax collection, combating tax evasion and illicit financial flows, and developing local capital markets in national currency are essential levers for financing development more autonomously and resiliently. Initiatives like the African Continental Free Trade Area (AfCFTA) could, in the long term, stimulate intra-African trade and reduce import dependence, thereby decreasing the need for foreign currency financing.

The debate on African debt is therefore changing in nature. It is no longer just about managing a "crisis," but about rethinking the rules of a global financial system that, in its current form, seems ill-suited to the challenges of the 21st century and the development aspirations of the African continent. The question is no longer whether Africa can repay its debt, but whether the world can afford not to invest in Africa's future.

The Term "African Debt Crisis" Amalgamates Opposing Situations

The term "African debt crisis" is a media shortcut that, by dint of repetition, ends up masking profoundly heterogeneous realities. By amalgamating the real distress situation of a handful of countries with the prudent management of many others, this single narrative produces two major perverse effects. Firstly, it stigmatizes the entire continent to international investors, reinforcing the unjustified risk premium that weighs on all African borrowers, including the most virtuous. Secondly, it dilutes the attention and political resources that should be focused on countries urgently needing rapid and effective debt restructuring.

The slight decrease in the debt ratio in 2025 is a weak signal, but it goes against the prevailing discourse of an uncontrollable spiral. The real issue is not so much the amount of debt as the conditions under which Africa accesses it. The exorbitant cost of borrowing, the biases of rating agencies, and the volatility of exchange rates are the real poisons. The discussion on African debt is, in reality, a discussion about the structural inequalities of the global financial architecture. The fight of African leaders for a reform of this system is not a request for assistance, but a demand for economic justice. It is the sine qua non for the continent to finance its own development and for the next decade not to be a lost decade, like the 1980s were.

---

Sources

- https://www.lebrief.ma/afrique/dette-publique-en-afrique-un-reflux-progressif-mais-des-niveaux-encore-eleves-100143497/

- _blank

- noopener

- Public Debt in Africa: A Gradual Retreat but Still High Levels.

- https://economic-research.bnpparibas.com/Media-Library/en-US/Saharan-Africa-public-debt-stabilises-vulnerabilities-increase-1/27/2026,c44631

- _blank

- noopener

- In sub-Saharan Africa, public debt stabilises but vulnerabilities increase.

- https://odi.org/en/insights/sub-saharan-africas-steep-debt-service-burden/

- _blank

- noopener

- Sub-Saharan Africa's steep debt service burden.

- https://www.agenceecofin.com/actualites/0203-136247-dette-publique-lafrique-confirme-son-desendettement-progressif-en-2025-malgre-un-record-mondial-iff

- _blank

- noopener

- Africa Confirms its Progressive Debt Reduction in 2025.

- https://www.afd.fr/fr/actualites/dette-afrique-economie-africaine

- _blank

- noopener

- Public Debt Becomes a Major Issue Again in Sub-Saharan Africa

- https://africarenewal.un.org/fr/magazine/le-dilemme-de-la-dette-en-afrique-transformer-la-crise-en-reforme

- _blank

- noopener

- Africa's Debt Dilemma: Turning Crisis into Reform

- https://fr.tradingeconomics.com/country-list/government-debt-to-gdp?continent=africa

- _blank

- noopener

- Government Debt to GDP - Country List - Africa

- The Perception Bias: An Obstacle to Development Financing in Africa