The Debt Spiral: A Ticking Time Bomb for Global Development

Developing countries' debt is reaching record levels, creating a net transfer of wealth to creditors and threatening essential public services. While global debt is expected to approach 100% of global GDP by 2030, restructuring mechanisms are struggling to provide effective solutions, as illustrated by the cases of Zambia, Sri Lanka, and Ghana.

A growing financial burden

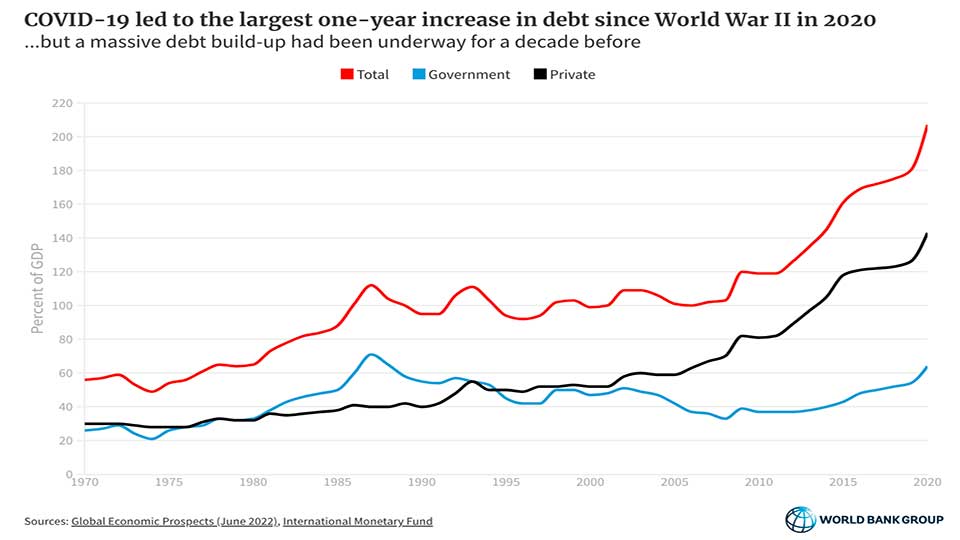

The global economy is facing a considerable accumulation of public debt, a trend that has accelerated over the past decade. The International Monetary Fund (IMF) projects that global public debt will approach 100% of Gross Domestic Product (GDP) by the end of the decade, a level that raises questions about long-term financial stability [2]. This situation is particularly pronounced in low- and middle-income countries, where the debt burden has reached critical proportions. According to World Bank data, the combined external debt of these nations peaked at a historic high of $8.9 trillion in 2024 [1].

This mountain of debt is not just an abstract figure; it translates into concrete and immediate consequences for the populations concerned. One of the most worrying aspects is the reversal of financial flows. Between 2022 and 2024, payments made by developing countries for their external debt service exceeded the amount of new financing they received by $741 billion [1]. This phenomenon constitutes a net transfer of wealth from the poorest economies to their creditors, whether they are multilateral institutions, governments, or private actors. This money, which leaves the indebted countries, is sorely needed to finance vital sectors. For the 78 most vulnerable countries, eligible for aid from the International Development Association (IDA), debt reached $1.2 trillion, and interest payments alone amounted to $415 billion in 2024 [1].

These colossal sums diverted from state budgets have a direct impact on the ability of governments to provide basic services. In the 22 most heavily indebted countries, it is estimated that 56% of the population cannot afford a healthy and nutritious diet [22]. Debt service thus enters into direct competition with spending on health, education, and climate change adaptation. Every dollar spent on repaying a loan is a dollar that is not invested in building a school, financing a hospital, or setting up resilient irrigation systems. This situation not only compromises the current well-being of citizens but also mortgages the long-term development prospects of these nations.

The G20 Common Framework: an ineffective solution?

Faced with the rising risks of over-indebtedness, the world's major economies have attempted to put in place coordinated resolution mechanisms. In November 2020, the G20, in collaboration with the Paris Club, launched the "Common Framework for Debt Treatments beyond the Debt Service Suspension Initiative (DSSI)" [3]. The objective was to provide a structured approach to the restructuring of the debt of eligible low-income countries, bringing together for the first time the traditional creditors of the Paris Club and the new major bilateral creditors, notably China.

The functioning of the Common Framework is based on several principles. The process is initiated by a debtor country which, faced with an unsustainable debt, requests a debt treatment within the framework of an IMF program. A committee of official creditors is then formed to negotiate the terms of a restructuring aimed at restoring debt sustainability. A fundamental principle is that of "comparability of treatment". It requires that private creditors and other bilateral creditors who are not members of the Paris Club grant debt relief at least as favorable as that granted by the committee of official creditors [3]. This clause aims to ensure a fair sharing of the burden of relief and to prevent some creditors from benefiting from the concessions made by others.

Despite these intentions, the implementation of the Common Framework has proved to be slow and complex. The process lacks clear and binding deadlines, which has led to significant delays in concluding agreements. Coordination between a diversity of creditors with heterogeneous interests and practices, including Chinese development banks, private investment funds, and sovereign bondholders, has proved to be particularly arduous. These difficulties have created great uncertainty for debtor countries, prolonging periods of economic crisis and delaying their return to stability. The reluctance of some countries to use the Framework, for fear of a downgrade in their credit rating and a loss of access to financial markets, has also limited its scope. The experiences of countries like Zambia have highlighted the structural limitations of this mechanism, sparking a debate on the need to reform it in depth.

Contrasting lessons from restructuring

The analysis of concrete cases of sovereign debt restructuring offers an insight into the strengths and weaknesses of the current international financial architecture. Zambia, the first African country to default on its debt in the midst of the COVID-19 pandemic in December 2020, has become an emblematic case study of the difficulties of the G20 Common Framework. The process of restructuring its debt has stretched over more than three and a half years [4]. This slowness has had severe economic consequences for the country, paralyzing investment and worsening the living conditions of the population. The long negotiations were marked by persistent disagreements between official creditors, notably China, and private bondholders, each seeking to minimize their losses and ensure that the others contribute equitably.

The case of Sri Lanka, although not eligible for the Common Framework, is also instructive. The country defaulted in 2022, caught in a major economic and political crisis. The structure of its debt was particularly complex, with a large share held by non-traditional creditors and a large component of domestic debt [5]. This fragmentation made negotiations even more difficult, requiring separate discussions with multiple groups of creditors. The process highlighted the absence of a global and orderly mechanism capable of managing complex sovereign defaults outside the limited scope of the Common Framework.

Conversely, the experience of Ghana offers a different perspective. Faced with an unsustainable debt, the Ghanaian government made the strategic decision to include its domestic debt in the scope of the restructuring from the beginning of the process [6]. This approach, although politically sensitive because it affects local investors and domestic banks, has made it possible to broaden the basis for burden sharing. By simultaneously dealing with external and internal debt, Ghana was able to present a more complete and balanced restructuring plan, which facilitated and accelerated the obtaining of an agreement with its external creditors within the framework of the Common Framework. This strategy allowed for a faster resolution than for Zambia, although questions remain about the long-term impact of the restructuring of domestic debt on the stability of the Ghanaian financial system. These three distinct trajectories demonstrate that there is no single solution and that the success of a restructuring depends on a multitude of factors, including the structure of the debt, the composition of the creditors, and the political choices of the debtor country.

Towards a new global debt architecture

The current sovereign debt crisis highlights the urgency of rethinking resolution mechanisms. The slowness and blockages observed within the G20 framework, as well as the difficulties encountered by countries like Sri Lanka, show that the current tools are not up to the task. Several avenues for reform are being considered to create a faster, fairer, and more effective system. One of the central proposals is to improve the Common Framework by integrating clear deadlines for each stage of the process, in order to prevent negotiations from dragging on. Greater transparency on the terms of loans, particularly on the part of all bilateral creditors, is also considered a necessary condition for facilitating debt sustainability analyses and ensuring effective comparability of treatment.

Some economists and civil society organizations are advocating for the establishment of a more formal and legally binding sovereign debt restructuring mechanism (SDRM), under the aegis of a neutral institution such as the United Nations. Such a mechanism could function as a kind of bankruptcy court for states, capable of imposing a solution on all creditors and suspending legal proceedings for the duration of the negotiations. This idea, which is not new, however, faces strong political resistance from some creditor countries and the private financial sector, who fear a challenge to the enforceability of loan contracts.

Beyond restructuring mechanisms, preventing debt crises is just as fundamental. This requires development financing that prioritizes grants and concessional loans for the poorest countries, as well as the development of more resilient debt instruments. Conditional clauses could, for example, provide for an automatic suspension of debt service in the event of a natural disaster or pandemic. Finally, the question of shared responsibility between lenders and borrowers is at the heart of the debate. Stricter regulation of sovereign lending could help to avoid the cycles of unsustainable debt that compromise development efforts and global economic stability. Resolving the debt crisis is not just a technical and financial issue; it is an imperative for achieving the Sustainable Development Goals and ensuring shared prosperity.

Sources

- [1] World Bank. External debt repayments of developing countries, worldbank.org

- [2] IMF. The rise in global debt, imf.org

- [3] Paris Club. The G20 Common Framework, clubdeparis.org

- [4] Center for Global Development. Zambia: Sovereign Debt Restructuring, cgdev.org

- [5] IMF. Sri Lanka's Sovereign Debt Restructuring, imf.org

- [6] Harvard Kennedy School. Ghana: Sovereign Debt Restructuring, hks.harvard.edu