AI as the Engine of Global Trade: One Third of Growth in 2025

# AI as a Driver of Global Trade: One-Third of 2025 Growth

Pillar : Economy & Innovation | Format : In-depth article | Date : March 20, 2026

---

In 2025, global trade grew faster than the world economy — and one-third of this growth came from a single sector: semiconductors and AI-related data center equipment. This is one of the conclusions of the McKinsey Global Institute's annual report on the geopolitics and geometry of global trade, published on March 19, 2026. The study, which covers over 90% of global trade across the ASEAN economies, Brazil, China, the European Union, India, the United States, and their partners, documents a profound reshaping of trade flows — in which AI now plays a central role.

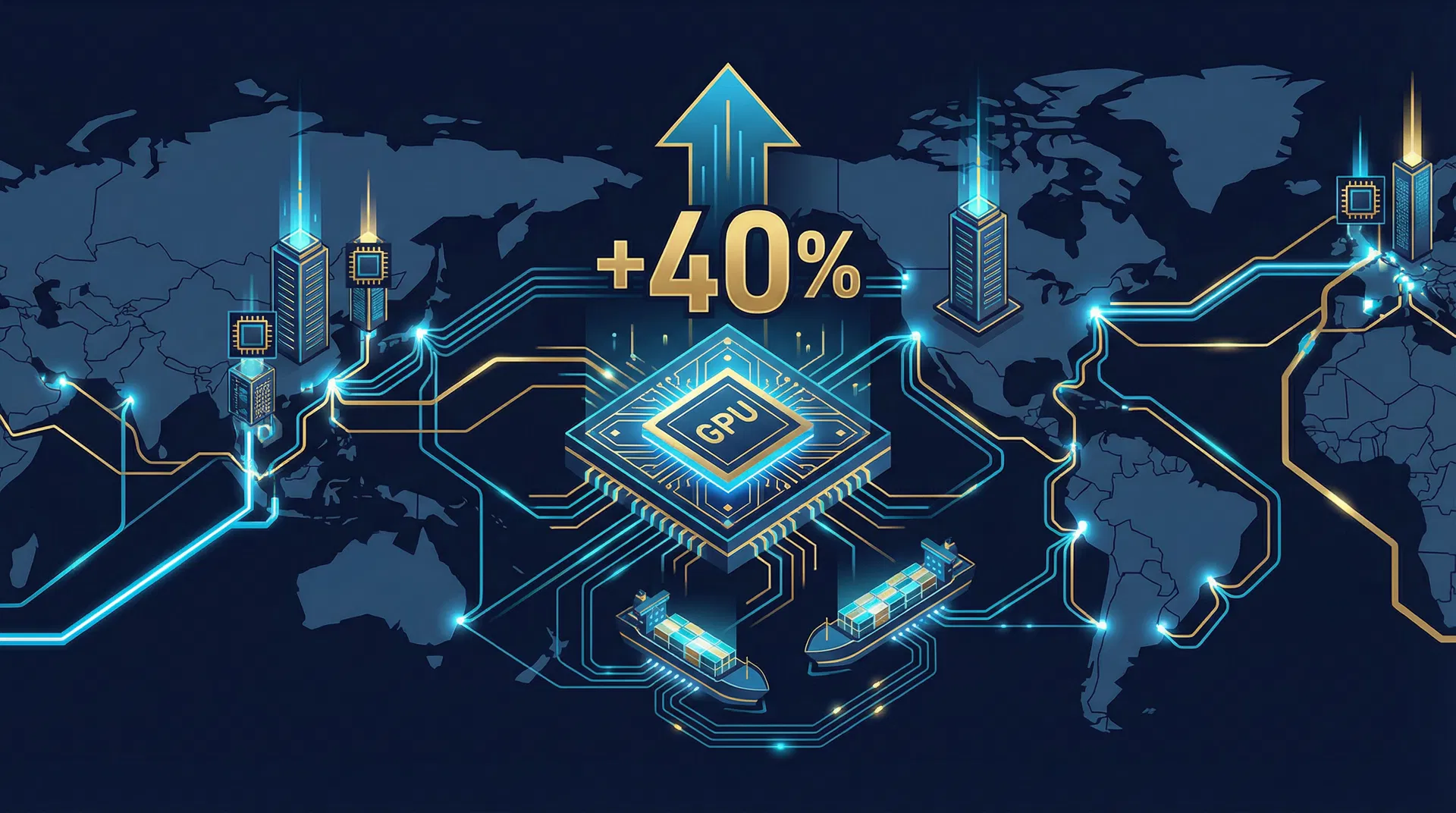

Semiconductors +40%, Global Trade +6.5%: AI Drives Growth Single-Handedly

Exports of semiconductors and data center equipment increased by approximately 40% in 2025, compared to a global trade average of 6.5%. This sector, which already accounted for a significant share of global trade, became the primary driver of trade growth for the year — surpassing energy, consumer goods, and raw materials.

Asian hubs were the major beneficiaries of this dynamic. Taiwan, South Korea, and several Southeast Asian economies supplied global markets, particularly the United States, with components and equipment necessary for AI infrastructure deployment. U.S. demand for servers, GPUs, and data center cooling equipment was particularly strong, fueled by massive investments from hyperscalers (Microsoft, Google, Amazon, Meta) and AI startups.

| Sector | Export Growth in 2025 |

|---|---|

| Semiconductors and AI Equipment | ~+40% |

| Consumer Goods | ~+5% |

| Energy | ~-9% |

| Global Average | ~+6.5% |

China, the "Factory of Factories"

The other structural trend documented by McKinsey is the evolution of China's role in global trade. Constrained by U.S. tariffs and restrictions on advanced semiconductor exports, China has accelerated its move upmarket in industrial components and capital goods destined for emerging economies.

McKinsey describes this phenomenon as China's transformation into the "factory of factories": it no longer merely supplies consumer goods to end markets but provides machinery, components, and equipment to growing manufacturing hubs — Vietnam, Indonesia, Mexico, India. This evolution is partly forced (U.S. restrictions pushed it to seek new markets) and partly strategic (China aims to establish itself as an indispensable supplier to global industrial value chains).

Chinese consumer goods exports to the United States plummeted by approximately 30% in 2025, due to tariffs. Chinese exporters responded by reducing their prices by an average of 8% to find buyers in new markets — Europe, Africa, Latin America. This redirection strategy partially offset the loss of the U.S. market.

From 2.4% to 22% in Four Months: The 2025 U.S. Tariff Shock

McKinsey's report details the evolution of U.S. tariffs in 2025. The average effective rate surged from 2.4% at the end of 2024 to approximately 22% in April 2025 — its highest level in a century. A series of bilateral agreements (with the United Kingdom, the EU, Vietnam, Japan, South Korea, India) brought this rate back down to around 15% by year-end. For China, the average effective annual rate was about 31%, with a peak of 137% in April.

The United States replaced approximately two-thirds of lost Chinese imports with imports from other suppliers. ASEAN was the major beneficiary of this redirection, simultaneously increasing its trade with both economies. The European Union, however, faced double pressure: more low-priced Chinese imports on its market and higher U.S. tariffs on its exports to the United States.

In February 2026, the U.S. Supreme Court invalidated the legal basis for certain tariffs introduced in 2025, leading to new measures under different legal authorities. The tariff situation remains in flux at the time of the report's publication.

The EU in a Vice

The European Union's position in this new trade landscape is particularly uncomfortable. It faces a dual competition: from Chinese exporters who, deprived of the U.S. market, are seeking alternative outlets in Europe, and from American producers who benefit from a protected domestic market and massive subsidies (IRA, CHIPS Act).

In the electric vehicle sector, the pressure is particularly evident. Chinese manufacturers, who have reduced their prices to offset the loss of the U.S. market, are offering models at prices that European manufacturers struggle to match. European customs duties on Chinese electric vehicles (introduced in 2024) partially cushioned the blow but did not resolve the structural competitiveness problem.

In the semiconductor and AI sector, Europe is absent from the list of winners. Neither a major supplier of AI equipment (like Taiwan or South Korea) nor a large deployment market on the same scale as the United States or China, the EU risks finding itself in a position of increasing dependence on the two blocs.

AI as a Geopolitical Reshaping Factor in Trade

McKinsey's report emphasizes that the growth of AI-related trade is not a geopolitically neutral phenomenon. Advanced semiconductors have been at the heart of tensions between the United States and China since 2022. U.S. restrictions on exporting advanced chips to China (NVIDIA H100, A100, and their successors) have pushed China to accelerate its own semiconductor development programs — with mixed results, but real progress.

The semiconductor value chain is one of the most geographically concentrated in global trade. Design is dominated by American companies (NVIDIA, AMD, Qualcomm, Intel) and a few European players (ASML, which manufactures the lithography machines essential for producing the most advanced chips). Manufacturing is concentrated in Taiwan (TSMC) and South Korea (Samsung, SK Hynix). This concentration creates systemic vulnerabilities that major powers seek to reduce — with massive investments in the United States (CHIPS Act: 52 billion dollars), Europe (European Chips Act: 43 billion euros), and China (several hundred billion yuan).

Vietnam +25%, ASEAN the Big Winner: The "Connector Trade" Reshaping Flows

One of the most striking findings of the McKinsey report is the emergence of ASEAN as the primary beneficiary of the reshaping of trade flows. The ten member countries of the Association of Southeast Asian Nations — Vietnam, Indonesia, Thailand, Malaysia, Philippines, Singapore, Myanmar, Cambodia, Laos, Brunei — simultaneously increased their trade with both major powers.

Vietnam is the most spectacular example. Its exports to the United States increased by approximately 25% in 2025, while Chinese exports to the United States fell. Vietnam has become an assembly hub for products previously manufactured in China — electronics, textiles, footwear. However, it imports a large portion of its components from China, meaning China indirectly benefits from the growth of Vietnamese exports to the United States. McKinsey calls this phenomenon "connector trade": ASEAN countries serve as connectors between the two major powers, absorbing flows that can no longer circulate directly.

Singapore, a financial and logistics hub in the region, benefited from an increase in capital and service flows related to the reshaping of supply chains. Indonesia, with its nickel and cobalt resources essential for electric batteries, attracted massive investments from China, the United States, and Europe in its processing capabilities.

This rise of ASEAN in global trade is a structural trend, not a cyclical phenomenon. The region combines an abundant and relatively inexpensive workforce, a strategic geographical position, and sufficient political stability to attract investment. If trade tensions between the United States and China persist, ASEAN is expected to continue benefiting from the diversification of supply chains.

Supreme Court Invalidates Tariffs, Situation Remains in Flux: What 2025 Data Doesn't Yet Cover

McKinsey's report covers data up to the end of 2025. Several developments in early 2026 could alter the documented trajectory. The U.S. Supreme Court's decision on tariffs, new tariff measures announced in 2026, and the evolution of trade negotiations between the United States and its partners create significant uncertainty for the short-term trajectory.

McKinsey also emphasizes that structural trends — the growth of AI-related trade, the rise of emerging markets, and the increasing role of geopolitics in trade decisions — are "durable" and not "flashes in the pan." AI as a driver of global trade is not a phenomenon unique to 2025: it is a fundamental trend that has accelerated and is expected to continue as AI infrastructure deployment intensifies.

ASML, Only European Player in a Strong Position: The Question of Structural Dependence

The central question for the coming years is whether the growth of AI-related trade will spread geographically — benefiting a greater number of economies — or remain concentrated in a few Asian hubs and the U.S. market. The answer will depend partly on industrial policies (who invests in what), partly on demand dynamics (which markets are deploying AI on a large scale), and partly on geopolitical decisions (which export restrictions are maintained or strengthened).

For Europe, the challenge is to define a position in this reshaping — neither a mere consumer of imported AI nor a marginal player in a value chain dominated by the United States and Asia. The Dutch ASML, which manufactures the EUV lithography machines essential for producing the most advanced chips, is the only European player in a structurally strong position within this chain. This is a considerable geopolitical asset — and a dependency that other players are actively seeking to reduce.

---

Sources

1. McKinsey Global Institute (2026, March 19). Geopolitics and the geometry of global trade: 2026 update. https://www.mckinsey.com/mgi/our-research/geopolitics-and-the-geometry-of-global-trade-2026-update

2. Yale Budget Lab (2026, January 19). State of U.S. Tariffs. https://budgetlab.yale.edu/research/state-us-tariffs-january-2026

3. World Trade Organization (2026). Regional Trade Agreements Database. https://www.wto.org/english/tratop_e/region_e/region_e.htm

4. World Economic Forum (2026, March 18). "Globalization's shift towards resilience and regions." https://www.weforum.org/stories/2026/03/globalization-rebuilt-around-resilience-regions-and-intelligence/

5. International Banker (2026, March 6). "Global Trade Shifts Ahead in 2026." https://internationalbanker.com/finance/global-trade-shifts-ahead-in-2026/